Terrible month with a $22k drop in investments due to the Iran conflict and resulting oil crisis, leading to shares taking a rather big dump. However, overall only a 4% dip which is good all things considering.

| Kiwisavers (Pensions) | Milford Growth Fund (Pensions) | Savings + Term Deposits | Shares | Bitcoin | Combined | |

| Total Value | 98,949 | 236,873 | 31,054 | 125,546 | 11,434 | 503,855 |

| $ Change | -4,892 | -14,058 | -3,692 | -941 | 1,514 | -22,070 |

| % Increase | -4.94% | -5.94% | -11.89% | -0.75% | 13.24% | -4.38% |

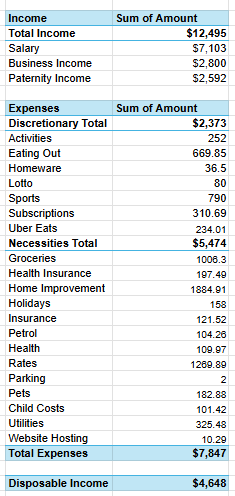

Income and Expenditure (approx)

The total income for the period is $12,495, primarily driven by salary income of $7,103, with additional contributions from business income ($2,800) and paternity income ($2,592).

Total expenses amount to $7,847, which are split between necessities ($5,474) and discretionary spending ($2,373). Necessary costs represent the larger share of expenditure, reflecting core living and household needs. The most significant expense categories include home improvement ($1,884.91), rates ($1,269.89), utilities ($325.48), and health-related costs, including health insurance and general health expenses.

Discretionary spending is mainly concentrated in sports ($790) and eating out ($669.85), alongside subscriptions and lifestyle costs such as activities and Uber Eats. Overall, discretionary expenses are moderate relative to income and appear controlled.

After all expenses, the remaining disposable income is $4,648, indicating a healthy surplus.