Good result for February 2026, with a total increase in investments of $10,433 which represents a 2.02% increase. Primarily driven by an increase in shares 16.42% (self managed). However, as can be seen below, we moved a significant amount of our savings into shares which boosts this number.

| Kiwisavers (Pensions) | Milford Growth Fund (Pensions) | Savings + Term Deposits | Shares | Bitcoin | Combined | |

| Total Value | 103,841 | 250,931 | 34,746 | 126,487 | 9,920 | 525,925 |

| $ Increase | 2,711 | 706 | -8,965 | 17,843 | -1,862 | 10,433 |

| % Increase | 2.68% | 0.28% | -20.51% | 16.42% | -15.80% | 2.02% |

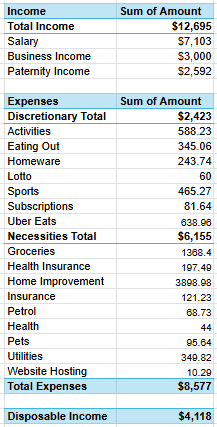

Income and Expenditure (approximate)

My total monthly income is $12,695, made up of salary ($7,103), business income ($3,000), and paternity income ($2,592).

My total monthly expenses come to $8,577, leaving me with $4,118 in disposable income.

The biggest portion of my spending is necessities ($6,155) — mainly home improvement ($3,898) which were two new heatpumps for the house, groceries ($1,368), and insurance-related costs. My discretionary spending totals $2,423, with sports ($1,065) and Uber Eats ($639) being the largest categories. Far too much on Uber Eats but it’s been a life safer when we’re in the trenches with a newborn and some days we’re knackered.

Overall, a fairly good month with income exceeding expenditure by $1k per week.

Net worth up by $10.4k over the month. Pretty happy with that outcome for now , but opportunity exists to increase both income and reduce expenses.